filmov

tv

Expected Shortfall

0:11:52

Expected Shortfall & Conditional Value at Risk (CVaR) Explained

0:08:44

Expected Shortfall Clearly Explained | FRM Part 1 |Valuation and Risk Models Book 4

0:04:42

Understanding Expected Shortfall (ES): A Comprehensive Guide

0:14:01

Expected Shortfall: An Introduction (FRM Part 1, Book 4, Valuation and Risk Models)

0:17:04

Expected shortfall (ES, FRM T5-02)

0:09:36

Conditional Value-at-Risk (Expected shortfall) - measuring expected extreme loss (Excel) (SUB)

0:01:41

Expected Shortfall Excel Spreadsheet

0:07:11

Expected Shortfall calculation using Excel

0:03:34

Mastering Conditional Value-at-Risk (CVaR) / Expected Shortfall

0:09:41

The importance of VaR and Expected Shortfall

0:16:26

Expected Shortfall for Discrete Distribution - Solved Example (FRM Part 1, FRM Part 2)

0:01:02

Expected Shortfall in the Normal distribution

0:06:00

Expected Shortfall | FRTB

0:18:20

Measures of Financial Risk (FRM Part 1 2025 – Book 4 – Chapter 1)

0:09:02

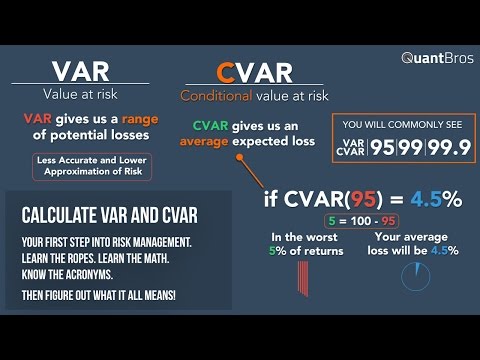

Calculating VAR and CVAR in Excel in Under 9 Minutes

0:32:13

Expected shortfall: approximating continuous, with code (ES continous, FRM T5-03)

0:08:08

Expected Shortfall for Uniform Distribution (Solved Example)(FRM Part 1, Valuation and Risk Models)

0:02:02

What Is Shortfall Risk?

0:06:01

FRM - Part 1 - Book 4 -Value at Risk & Expected Shortfall -Coherent Risk Measure - Subadditivity

0:03:47

Computing the Expected Shortfall - Portfolio and Risk Management

0:01:58

FRM Part 1 Calculate Value at Risk and Expected Shortfall

0:05:09

Value at Risk Explained in 5 Minutes

0:06:50

FRM Part 1 - Historical Simulation - Value at Risk (VaR) and Expected Shortfall #frm

0:12:19

Chapter 9 part 4

Вперёд

0:11:52

0:11:52

0:08:44

0:08:44

0:04:42

0:04:42

0:14:01

0:14:01

0:17:04

0:17:04

0:09:36

0:09:36

0:01:41

0:01:41

0:07:11

0:07:11

0:03:34

0:03:34

0:09:41

0:09:41

0:16:26

0:16:26

0:01:02

0:01:02

0:06:00

0:06:00

0:18:20

0:18:20

0:09:02

0:09:02

0:32:13

0:32:13

0:08:08

0:08:08

0:02:02

0:02:02

0:06:01

0:06:01

0:03:47

0:03:47

0:01:58

0:01:58

0:05:09

0:05:09

0:06:50

0:06:50

0:12:19

0:12:19